Exam Details

Exam Code

:FINANCIAL-ACCOUNTING-AND-REPORTINGExam Name

:Financial ReportingCertification

:Test Prep CertificationsVendor

:Test PrepTotal Questions

:163 Q&AsLast Updated

:Apr 14, 2025

Test Prep Test Prep Certifications FINANCIAL-ACCOUNTING-AND-REPORTING Questions & Answers

-

Question 121:

In which of the following situations should a company report a prior-period adjustment?

A. A change in the estimated useful lives of fixed assets purchased in prior years.

B. The correction of a mathematical error in the calculation of prior years' depreciation.

C. A switch from the straight-line to double-declining balance method of depreciation.

D. The scrapping of an asset prior to the end of its expected useful life.

-

Question 122:

If a company is not presenting comparative financial statements, the correction of an error in the financial statements of a prior period should be reported, net of applicable income taxes, in the current:

A. Retained earnings statement after net income but before dividends.

B. Retained earnings statement as an adjustment of the opening balance.

C. Income statement after income from continuing operations and before extraordinary items.

D. Income statement after income from continuing operations and after extraordinary items.

-

Question 123:

The cumulative effect of a change in accounting estimate should be shown separately: A. On the income statement above income from continuing operations.

B. On the income statement after income from continuing operations and before extraordinary items.

C. On the retained earnings statement as an adjustment to the beginning balance.

D. It should not be recorded separately on any financial statement.

-

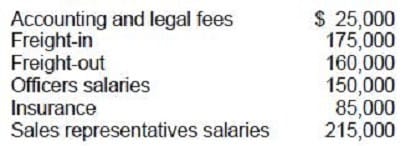

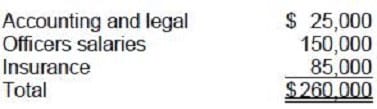

Question 124:

The following costs were incurred by Griff Co., a manufacturer, during 1992:

What amount of these costs should be reported as general and administrative expenses for 1992?

A. $260,000

B. $550,000

C. $635,000

D. $810,000

-

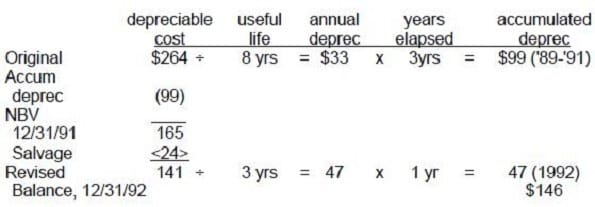

Question 125:

On January 2, 1989, Union Co. purchased a machine for $264,000 and depreciated it by the straight-line method using an estimated useful life of eight years with no salvage value. On January 2, 1992, Union determined that the machine had a useful life of six years from the date of acquisition and will have a salvage value of $24,000. An accounting change was made in 1992 to reflect the additional data. The accumulated depreciation for this machine should have a balance at December 31, 1992, of:

A. $176,000

B. $160,000

C. $154,000

D. $146,000

-

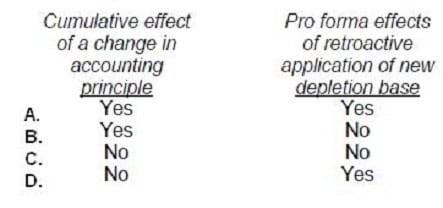

Question 126:

During 1992, Krey Co. increased the estimated quantity of copper recoverable from its mine. Krey uses the units of production depletion method. As a result of the change, which of the following should be reported in Krey's 1992 financial statements?

A. Option A

B. Option B

C. Option C

D. Option D

-

Question 127:

On November 1, 20X2, Smith Co. contracted to dispose of an industry segment. Throughout 20X2 the segment had operating losses. These losses were expected to continue until the segment's disposition. If a loss is projected on final disposition, how much of the operating losses should be included in the loss from discontinued operations reported in Smith's 20X2 income statement?

I. Operating losses for the period January 1 to October 31, 20X2.

II. Operating losses for the period November 1 to December 31, 20X2.

III.

Estimated operating losses for the period January 1 to February 28, 20X3.

A.

II only.

B.

II and III only.

C.

I and III only.

D.

I and II only.

-

Question 128:

During 1994, Orca Corp. decided to change from the FIFO method of inventory valuation to the weightedaverage method. Inventory balances under each method were as follows:

Orca's income tax rate is 30%.

Orca should report the cumulative effect of this accounting change as a(n):

A. Adjustment to beginning retained earnings.

B. Component of income from continuing operations.

C. Extraordinary item.

D. Component of income after extraordinary items.

-

Question 129:

A transaction that is unusual in nature and infrequent in occurrence should be reported separately as a component of income:

A. After cumulative effect of accounting changes and before discontinued operations of a segment of a business.

B. After cumulative effect of accounting changes and after discontinued operations of a segment of a business.

C. Before cumulative effect of accounting changes and before discontinued operations of a segment of a business.

D. After discontinued operations of a segment of a business.

-

Question 130:

How should the effect of a change in accounting estimate be accounted for?

A. By restating amounts reported in financial statements of prior periods.

B. By reporting pro forma amounts for prior periods.

C. As a prior period adjustment to beginning retained earnings.

D. In the period of change and future periods if the change affects both.

Related Exams:

AACD

American Academy of Cosmetic DentistryACLS

Advanced Cardiac Life SupportASSET

ASSET Short Placement Tests Developed by ACTASSET-TEST

ASSET Short Placement Tests Developed by ACTBUSINESS-ENVIRONMENT-AND-CONCEPTS

Certified Public Accountant (Business Environment amd Concepts)CBEST-SECTION-1

California Basic Educational Skills Test - MathCBEST-SECTION-2

California Basic Educational Skills Test - ReadingCCE-CCC

Certified Cost Consultant / Cost Engineer (AACE International)CGFM

Certified Government Financial ManagerCGFNS

Commission on Graduates of Foreign Nursing Schools

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only Test Prep exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your FINANCIAL-ACCOUNTING-AND-REPORTING exam preparations and Test Prep certification application, do not hesitate to visit our Vcedump.com to find your solutions here.