Certified Public Accountant (Business Environment amd Concepts)

Exam Details

Exam Code

:BUSINESS-ENVIRONMENT-AND-CONCEPTS

Exam Name

:Certified Public Accountant (Business Environment amd Concepts)

Certification

:Test Prep Certifications

Vendor

:Test Prep

Total Questions

:530 Q&As

Last Updated

:Apr 11, 2025

Test Prep Test Prep Certifications BUSINESS-ENVIRONMENT-AND-CONCEPTS Questions & Answers

Question 141:

Which of the following effects would a lockbox most likely provide for receivables management?

A. Minimized collection float.

B. Maximized collection float.

C. Minimized disbursement float.

D. Maximized disbursement float.

Correct Answer: A

Choice "a" is correct. A lockbox system expedites cash inflows (minimizes collection float) by having a

bank receive payments from a company's customers directly, via mailboxes to which the bank has access.

Payments that arrive in these mailboxes are deposited into the company's account immediately.

Choice "b" is incorrect. Lockboxes minimize rather than maximize collection float.

Choices "c" and "d" are incorrect. Lockbox systems relate to collection rather than disbursement float.

Question 142:

The CFO of a company is concerned about the company's accounts receivable turnover ratio. The company currently offers customers terms of 3/10, net 30. Which of the following strategies would most likely improve the company's accounts receivable turnover ratio?

A. Pledging the accounts receivable to a finance company.

B. Changing customer terms to 1/10, net 30.

C. Entering into a factoring agreement with a finance company.

D. Changing customer terms to 3/20, net 30.

Correct Answer: C

Choice "c" is correct. The accounts receivable turnover ratio is expressed as Sales ?Accounts Receivable. A reduction in accounts receivable would serve to improve (increase) the turnover ratio. Factoring (selling) receivables would serve to reduce the amount of accounts receivable (indicating more rapid collections) thereby increasing (improving) the company's accounts receivable. Choice "a" is incorrect. Pledging accounts receivable does not impact either sales or accounts receivable. There would be no improvement in the accounts receivable turnover ratio. Choice "b" is incorrect. Changing the customer terms from 3/10, net 30 to 1/10, net 30 would actually reduce discount incentives to pay timely. Accounts receivable would likely remain the same or be higher. There would be no improvement in the company's accounts receivable turnover ratio. Choice "d" is incorrect. Changing the customer terms from 3/10, net 30 to 3/20, net 30 would actually reduce incentives to pay timely by increasing the amount of time in which the customer could capitalize on the discount. Accounts receivable would likely remain the same or be higher. There would be no improvement in the company's accounts receivable turnover ratio.

Question 143:

Why would a firm generally choose to finance temporary assets with short-term debt?

A. Matching the maturities of assets and liabilities reduces risk.

B. Short-term interest rates have traditionally been more stable than long-term interest rates.

C. A firm that borrows heavily long term is more apt to be unable to repay the debt than a firm that borrows heavily short term.

D. Financing requirements remain constant.

Correct Answer: A

Choice "a" is correct. Matching the maturities of current assets with liabilities as they come due is designed to ensure liquidity and reduce risk of cash shortages. Temporary assets (such as inventories, generally, and seasonal inventories, specifically) might be financed with short term debt such that the earnings from the sales of those temporary assets could be used to liquidate the related obligations as they come due and ensure that cash is available to meet cash flow requirements. Choice "b" is incorrect. Interest rate risks would likely motivate a firm to use longer term financing than short-term financing. Choice "c" is incorrect. Matching cash inflows with cash outflows are more influential in determining a firm's ability to repay debt rather than the length of the obligation. Choice "d" is incorrect. Long-term rather than short-term debt promotes consistent finance charges. The requirements for financing itself are driven by business practice, not by the maturity of financial instruments used.

Question 144:

Amicable Wireless, Inc. offers credit terms of 2/10, net 30 for its customers. Sixty percent of Amicable's customers take the 2% discount and pay on day 10. The remainder of Amicable's customers pay on day

30. How many days' sales are in Amicable's accounts receivable?

A. 6

B. 12

C. 18

D. 20

Correct Answer: C

Choice "c" is correct. Days' sales in accounts receivable is normally calculated as Days' sales = Ending accounts receivable / Average daily sales. However, that formula will not work in this case because the necessary information is not provided. However, enough information about payments is provided so that the total days' sales can be determined on a weighted average basis. In this question, nobody pays before the 10th day and 60% of the customers pay on the 10th day, so there are 10 x .60, or 6 day's sales there. The other 40% of the customers pay on the 30th day so there are 30 x .40, or 12 day's sales there. The total is 18 days sales.

Choice "a" is incorrect. This answer is apparently calculated from just the 60% of the customers who pay on the 10th day. The others have to be included also. Choice "b" is incorrect. This answer is apparently calculated from just the 40% of the customers who pay on the 30th day. The others have to be included also. Choice "d" is incorrect. This answer is apparently calculated by as the difference between the 30th day and the 10th day. The answer does not take into account how many customers pay when.

Question 145:

The benefits of a just-in-time system for raw materials usually include:

A. Elimination of nonvalue adding operations.

B. Increase in the number of suppliers, thereby ensuring competitive bidding.

C. Maximization of the standard delivery quantity, thereby lessening the paperwork for each delivery.

D. Decrease in the number of deliveries required to maintain production.

Correct Answer: A

Choice "a" is correct. The just-in-time system focuses on expediting the production process by having materials available as needed without having to store them prior to usage. Thus, the nonvalue adding operation of storing materials is eliminated. Choice "b" is incorrect. A just-in-time system is designed to facilitate the flow of materials whether the materials come from one or more suppliers. Competitive bidding is not a major benefit of the just-in-time system. Choice "c" is incorrect. Maximizing the delivery quantity of materials may increase the need to store the materials prior to using them. The just-in-time system focuses on minimizing storage time and storage costs. Lessening paperwork is not a focus of the just-in-time system. Choice "d" is incorrect. With a just-in-time system, deliveries are made as materials are needed. A decrease in deliveries may increase the delivery quantity, thus increasing the need to store the materials prior to using them. The just-in-time system focuses on minimizing storage time and storage costs.

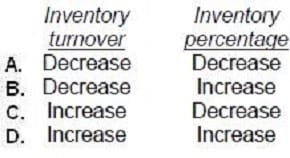

Question 146:

Bell Co. changed from a traditional manufacturing philosophy to a just-in-time philosophy. What are the expected effects of this change on Bell's inventory turnover and inventory as a percentage of total assets reported on Bell's balance sheet?

A. Option A

B. Option B

C. Option C

D. Option D

Correct Answer: C

Choice "c" is correct. In a just-in-time system, products are produced just-in-time to be sold. Therefore, JIT systems maintain a much smaller level of inventory when compared to traditional systems. Inventory turnover (cost of goods sold divided by average inventory) increases with a switch to JIT, and inventory as a percentage of total assets decreases. Choices "a", "b", and "d" are incorrect based on the above Explanation.

Question 147:

Which of the following is not a typical characteristic of a just-in-time (JIT) production environment?

A. Lot sizes equal to one.

B. Insignificant setup times and costs.

C. Push-through system.

D. Balanced and level workloads.

Correct Answer: C

Choice "c" is correct. Just-in-time has the goal to minimize the level of inventory carried. Typical

characteristics include lot sizes equal to one, insignificant set-up times and costs, and balanced and level

workloads. In a just-in-time environment, the flow of goods is controlled by a "pull" approach, where an

item is produced only when it is needed down the line, and not a "push-through" system.

Choices "a", "b", and "d" are incorrect based on the above Explanation.

Question 148:

Which of the following ratios is appropriate for the evaluation of accounts receivable?

A. Days sales outstanding.

B. Return on total assets.

C. Collection to debt ratio.

D. Current ratio.

Correct Answer: A

Choice "a" is correct. Among the ratios listed, the ratio that is appropriate for the evaluation of accounts receivable is the number of days sales are outstanding. Sales are related to accounts receivable, so the more days the sales are outstanding, the longer the receivables are outstanding. Choice "b" is incorrect. Return on total assets is not appropriate for the evaluation of accounts receivable. It is appropriate for the evaluation of return and of total assets, but not for the evaluation of account receivable specifically. Choice "c" is incorrect. The collection to debt ratio has nothing to do with the evaluation of accounts receivable. Choice "d" is incorrect. The current ratio is appropriate for the evaluation of liquidity (one of the ways to evaluate liquidity) but has nothing to do with the evaluation of accounts receivable, other than that accounts receivable is in the numerator of the current ratio.

Question 149:

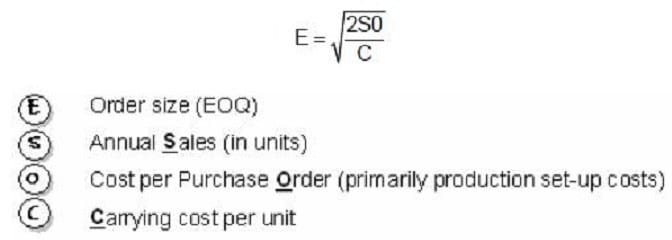

Which of the following inventory management approaches orders at the point where carrying costs equate nearest to restocking costs in order to minimize total inventory cost?

A. Economic order quantity.

B. Just-in-time.

C. Materials requirements planning.

D. ABC.

Correct Answer: A

Choice "a" is correct. The economic order quantity (EOQ) method of inventory control anticipates orders at the point where carrying costs are nearest to restocking costs. The objective of EOQ is to minimize total inventory costs. The formula for EOQ is: Choice "b" is incorrect. Just in time (JIT) inventory models were developed to reduce the lag time between inventory arrival and inventory use. Choice "c" is incorrect. Materials requirements planning (MRP) is a method of determining inventory requirements when a given number of units is needed. The method is used to create precise schedules of which items will be needed and what times they will be needed. Choice "d" is incorrect. ABC is an acronym for Activity Based Costing, a method of cost assignment that identifies value added activities and related cost drivers. It is not an inventory management approach.

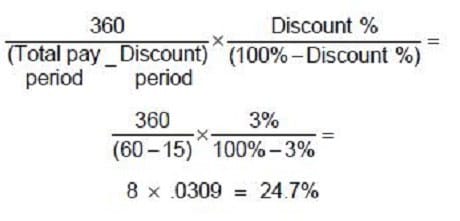

Question 150:

Quantree Company is quoted credit terms of 3/15, net 60 (using a 360-day year). The effective cost of not taking this discount and paying on day 60 is (rounded to nearest hundredth):

A. 24.74 percent.

B. 24.00 percent.

C. 18.56 percent.

D. 18.00 percent.

Correct Answer: A

Choice "a" is correct. The formula for computing the cost of credit discounts is:

Choices "b", "c", and "d" are incorrect, per the above calculation.

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only Test Prep exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your BUSINESS-ENVIRONMENT-AND-CONCEPTS exam preparations and Test Prep certification application, do not hesitate to visit our Vcedump.com to find your solutions here.