Exam Details

Exam Code

:FINANCIAL-ACCOUNTING-AND-REPORTINGExam Name

:Financial ReportingCertification

:Test Prep CertificationsVendor

:Test PrepTotal Questions

:163 Q&AsLast Updated

:Apr 14, 2025

Test Prep Test Prep Certifications FINANCIAL-ACCOUNTING-AND-REPORTING Questions & Answers

-

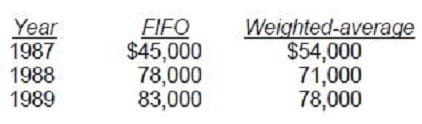

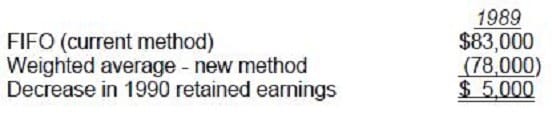

Question 51:

Goddard has used the FIFO method of inventory valuation since it began operations in 1987. Goddard decided to change to the weighted-average method for determining inventory costs at the beginning of 1990. The following schedule shows year-end inventory balances under the FIFO and weighted-average methods:

What amount, before income taxes, should be reported in the 1990 retained earnings statement as the

cumulative effect of the change in accounting principle?

A. $5,000 decrease.

B. $3,000 decrease.

C. $2,000 increase.

D. $0.

-

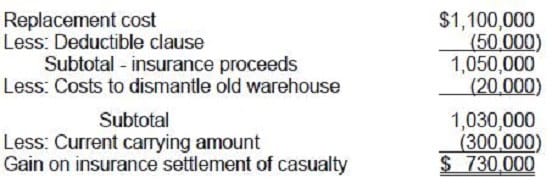

Question 52:

Ocean Corp.'s comprehensive insurance policy allows its assets to be replaced at current value. The policy has a $50,000 deductible clause. One of Ocean's waterfront warehouses was destroyed in a winter storm. Such storms occur approximately every four years. Ocean incurred $20,000 of costs in dismantling the warehouse and plans to replace it. The tax rate is 30%. The following data relate to the warehouse:

Current carrying amount $ 300,000 Replacement cost 1,100,000

What amount of gain should Ocean report as a separate component of income before extraordinary items?

A. $1,030,000

B. $780,000

C. $730,000

D. $0

-

Question 53:

Which of the following should be reported as a prior period adjustment?

A. Option A

B. Option B

C. Option C

D. Option D

-

Question 54:

On January 1, 20X1, Pell Corp. purchased a machine having an estimated useful life of 10 years and no salvage. The machine was depreciated by the double declining balance method for both financial statement and income tax reporting. On January 1, 20X6, Pell changed to the straight-line method for financial statement reporting but not for income tax reporting. Accumulated depreciation at December 31, 20X5, was $560,000. If the straight-line method had been used, the accumulated depreciation at December 31, 20X5, would have been $420,000. Pell's enacted income tax rate for 20X6 and thereafter is 30%. The amount shown in the 20X6 income statement for the cumulative effect of changing to the straight-line method should be:

A. $98,000 debit.

B. $98,000 credit.

C. $140,000 credit.

D. $0.

-

Question 55:

In 1990, Teller Co. incurred losses arising from its guilty plea in its first antitrust action, and from a substantial increase in production costs caused when a major supplier's workers went on strike. Which of these losses should be reported as an extraordinary item?

A. Option A

B. Option B

C. Option C

D. Option D

-

Question 56:

During 1990, Fuqua Steel Co. had the following unusual financial events occur:

•

Bonds payable were retired five years before their scheduled maturity, resulting in a $260,000 gain. Fuqua has frequently retired bonds early when interest rates declined significantly.

•

A steel forming segment suffered $255,000 in losses due to hurricane damage. This was the fourth similar loss sustained in a 5-year period at that location.

•

A component of Fuqua's operations, steel transportation, was sold at a net loss of $350,000.

This was Fuqua's first divestiture of one of its operating segments.

Before income taxes, what amount should be disclosed as the gain (loss) from extraordinary items in

1990?

A. $0

B. $5,000

C. $(90,000)

D. $(350,000)

-

Question 57:

Thorpe Co.'s income statement for the year ended December 31, 1990, reported net income of $74,100. The auditor raised questions about the following amounts that had been included in net income:

The loss from the fire was an infrequent but not unusual occurrence in Thorpe's line of business. Thorpe's December 31, 1990, income statement should report net income of:

A. $65,000

B. $66,100

C. $81,600

D. $87,000

-

Question 58:

A transaction that is unusual, but not infrequent, should be reported separately as a(an):

A. Extraordinary item, net of applicable income taxes.

B. Extraordinary item, but not net of applicable income taxes.

C. Component of income from continuing operations, net of applicable income taxes.

D. Component of income from continuing operations, but not net of applicable income taxes.

-

Question 59:

During 1990, Fuqua Steel Co. had the following unusual financial events occur:

•

Bonds payable were retired five years before their scheduled maturity, resulting in a $260,000 gain. Fuqua has frequently retired bonds early when interest rates declined significantly.

•

A steel forming segment suffered $255,000 in losses due to hurricane damage. This was the fourth similar loss sustained in a 5-year period at that location.

•

A component of Fuqua's operations, steel transportation, was sold at a net loss of $350,000.

This was Fuqua's first divestiture of one of its operating segments.

Before income taxes, what amount of gain (loss) should be reported separately as a component of income

from continuing operations in 1990?

A. $260,000

B. $5,000

C. $(255,000)

D. $(350,000)

-

Question 60:

Coffey Corp.'s trial balance of Income Statement Accounts for the year ended December 31, 1988 as follows:

Coffey's income tax rate is 30%. The gain on debt extinguishment is considered a usual and recurring part of Coffey's operations. The hurricane is considered an unusual and infrequent event. Coffey prepares a multiple-step income statement for 1988.

Net income is:

A. $140,000

B. $161,000

C. $168,000

D. $200,000

Related Exams:

AACD

American Academy of Cosmetic DentistryACLS

Advanced Cardiac Life SupportASSET

ASSET Short Placement Tests Developed by ACTASSET-TEST

ASSET Short Placement Tests Developed by ACTBUSINESS-ENVIRONMENT-AND-CONCEPTS

Certified Public Accountant (Business Environment amd Concepts)CBEST-SECTION-1

California Basic Educational Skills Test - MathCBEST-SECTION-2

California Basic Educational Skills Test - ReadingCCE-CCC

Certified Cost Consultant / Cost Engineer (AACE International)CGFM

Certified Government Financial ManagerCGFNS

Commission on Graduates of Foreign Nursing Schools

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only Test Prep exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your FINANCIAL-ACCOUNTING-AND-REPORTING exam preparations and Test Prep certification application, do not hesitate to visit our Vcedump.com to find your solutions here.